A “registered charity” is a technical and precise term referring to a charitable organization that is registered under the Income Tax Act (ITA). In order for your organization to be a registered charity, you must have applied for charitable status with the Charities Directorate of the Canada Revenue Agency (CRA).

Municipal, provincial (territorial), federal, and specific commissions and other bodies define the terms “charity” and “charitable” in various ways. Just because your organization is referred to as a “charity” or because you do “charitable” work (that is, helping those in need and not taking any profit) does not necessarily mean that your organization is a registered charity under the ITA.

Your organization can become a registered charity by applying for charitable status with the CRA. Detailed requirements are set out in the rules of the ITA. The process begins by sending in a completed T2050 form. When the process is complete, the federal government provides you with a charities registration number.

Don’t confuse a charities registration number with a fundraising registration number (issued by the province, territory, or municipality) or a corporate number (issued upon registration as a corporation).

A non-profit organization can be set up for any legal purpose as long as its members do not receive a direct financial benefit from the revenues or assets of the organization. A non-profit can operate fully without registering as a registered charity with the Canada Revenue Agency (CRA).

A registered charity, on the other hand, is a technical and precise term that refers to an organization that

More…

For further explanation of the differences between a registered charity and a non-profit organization, go to our Fast Fact on Registered Charity vs Non-Profit.

Short Answer

Not necessarily. Just because an organization uses the word “charitable” to describe itself and what it does, the organization is not necessarily a registered charity. An organization can run on a not-for-profit basis without registering as a registered charity with the Canada Revenue Agency (CRA). A “registered charity” is a technical and precise term referring to a charitable organization that is registered under the Income Tax Act (ITA).

Long Answer

Municipal, provincial (territorial), federal, and specific commissions and other bodies define the terms “charity” and “charitable” in various ways. Often, these definitions are not linked to the concept of a registered charity under the ITA.

As you can see, most provincial legislation uses the terms “charity” and “charitable” to refer to non-profit work in general and charitable works at an informal level. This does not mean that your organization is a registered charity for the purposes of the ITA and the CRA.

Short Answer

A charitable registration number is a number assigned by the Canada Revenue Agency (CRA) to a registered charity.

Long Answer

A charitable registration number has 12 digits and 2 letters. It consists of

Example

987654321RR0001 is an example of a charitable registration number

You may also be able to find this information

Short answer

Perhaps. First, a charity wishing to start new programs or activities should make sure that the new activities are in step with its objects. Then, it should consult the Charities Directorate of the Canada Revenue Agency (CRA) to check that the new program or activity is charitable and falls within the scope of the charity’s approved purposes (objects).

Long answer

Your charity should send the Charities Directorate a detailed description of the proposed program or activity, as well as any related promotional material (brochures, posters, or newsletters).

In some cases, a charity may have to alter its purpose so that it has a basis for taking on the new activities. If this is the case, after the charity has amended its purposes, it has to send the revised governing documents to the Charities Directorate. Detailed information on the process of changing a charity’s purposes can be found at Changing a Charity’s Purposes.

Short answer

No! Under no circumstances should your registration number be loaned to another organization.

Long answer

A charity is responsible for all tax receipts issued under its name and number and must account for the corresponding donations on its annual information return.

Lending the registration number to another organization could lead to the revocation of your charity’s registered status.

Short answer

“At arm’s-length” describes a relationship in which the parties act independently of each other.

The opposite —“not at arm’s-length”— includes individuals who are related to each other by blood, marriage, adoption, and common law relationships. Not at arm’s-length also covers people acting together without separate interests, such as those with close business ties.

Long answer

The concept of arm’s-length is used, amongst other things, in registered charities to clarify private benefit. For example, promotional items must be supplied at arm’s-length at a reasonable market value and without any excessive private benefit to the supplier, the charity’s board, or any individual members of the board.

Congratulations! You should begin by requesting revocation of your registered status from the Charities Directorate of the Canada Revenue Agency.

Once your charity’s status is revoked,

More…

If your charity is considering merging, amalgamating, or consolidating with another organization, you should consult with the Charities Directorate at 1-800-267-2384 (English) or 1-888-892-5667 (bilingual) before doing so.

For inquiries about registered charities, telephone:

A registered charity can make grants or gifts to other qualified donees or it can carry out its own activities or purposes as set out in its incorporation documents.

Yes. Even though most non-profit organizations are exempt from income tax, the organization must still complete an income tax return each year to report to Revenue Canada. The form that is completed will differ according to whether the organization is a registered charity or whether it is a non-profit that is not also a registered charity.

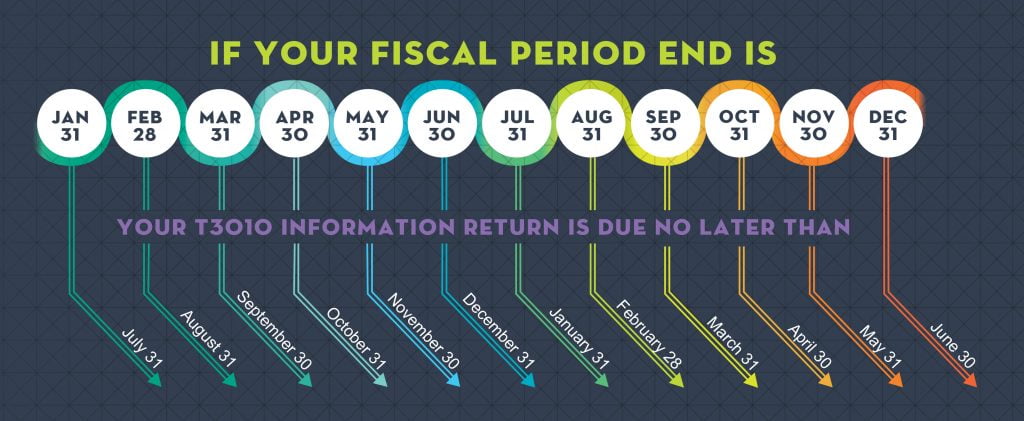

Registered charities must file a Form T3010 and financial statements within six months from the end of each fiscal period. For more information, see the Revenue Canada website at https://www.canada.ca/en/revenue-agency/services/charities-giving/charities.html

Other non-profits must file a T2 Corporation Income Tax Return. Many non-profits that are not registered charities will be able to complete the short version of the T2 annual return form if they have a permanent residence in only one province or territory. If they have a presence in more than one province or territory, the organization will have to complete a regular T2 Corporation Income Tax Return. These forms are available on the Revenue Canada website at https://www.canada.ca/en/revenue-agency/services/forms-publications.html/. This form serves as a federal, provincial, and territorial corporation income tax return, unless the corporation is located in Quebec or Alberta. If the corporation is located in one of these provinces, you have to file a separate provincial corporation return.

Your non-profit organization may have to complete the Form T1044, Non-Profit Organization (NPO) Information Return, if it is not a registered charity and if it meets one of the following conditions:

Some non-profit organizations are required to pay tax on income from property. This situation will arise when the main purpose of the organization is the provision of dining, recreational or sports facilities for its members. For more information, see the Revenue Canada site at www.cra-arc.gc.ca/E/pub/tp/it83r3/it83r3-e.html

For more information on non-profit organizations and taxes, see the Revenue Canada website at https://www.canada.ca/en/services/taxes/charities.html

Short Answer:

There is no legal requirement under the Income Tax Act that a Canadian charity have resident Canadian directors.

Long Answer

While there is no legal requirement under tax legislation for Canadian charities to have directors who live in Canada, the Income Tax Act requires that Canadian charities maintain direction and control over their own activities. For groups applying for charitable status or for charities who have obtained charitable status, this may be more difficult to prove where one or more of their directors are not resident in Canada. As well, if the charity is constituted as a corporation, the federal or provincial statute under which it was established or operates may specify certain residency requirements for directors.

More information

This website was made possible with a financial contribution from the Canada Revenue Agency to the Centre for Public Legal Education Alberta.

The Centre for Public Legal Education respectfully acknowledges that we are located on Treaty 4, 6, 7, 8 and 10 territories, the traditional lands of First Nations, Métis, and Inuit.